Representative image | Seth Moulton

In the context of increasing geopolitical tensions, where trade and investment are increasingly being repurposed from business decisions to instruments being wielded for national security, enhancing external engagement and expanding overseas investments emerge as critical imperatives for advancing India’s strategic interests.

Introduction

For developing countries which face a significant gap in available funding for investments in productive forces, attracting foreign direct investments (FDI) is a key policy priority and they aim to stimulate inward investments through a range of measures such as tax benefits, facilitative investment environments and better infrastructure. At the same time, corporations across the world attempt to derive business advantage by investing overseas to gain market share by being closer to their target customers or to acquire technologies for their future growth, resulting in the creation of global value chains spanning multiple sectors and countries.

The strategic role of outward direct investments (ODI), on the other hand, has been accorded a lower priority by policymakers in developing countries preferring to channelize available funds into the domestic economy. Nevertheless, corporations in these countries leverage overseas opportunities and address foreign markets for growth and diversification. At a national level, an effective ODI policy could be a potent option for strengthening global economic influence and enhancing strategic presence. Within a fraught geopolitical framework, where risks and challenges of investing overseas abound, governmental support would provide an effective backstop to investments.

Corporates from advanced economies represent the major proportion of global ODI, acknowledging the growth opportunities in other countries. Global fund outflows increased from USD 1 trillion in 2018 to USD 1.9 trillion in 2021, before declining to USD 1.56 trillion in 2023. Developing economies accounted for 37.3% of this aggregate in 2018, a figure which came down to 31.6% in 2023.

The US stood at top spot in outward flows of investment in 2023 at USD 404 billion. Japan was the second largest investor in 2023, followed by China (USD 148 billion), Switzerland (USD 105 billion) and Hong Kong (USD 104 billion). With a long history of being the largest outward investor, the US holds a cumulative FDI stock of USD 8 trillion from 1990-2022, with the Netherlands coming in second with USD 3.2 trillion and China with USD 2.9 trillion.

India, which ranked 23rd in the list of outward investing nations in 2022, improved its position to enter the top 20 list in 2023; however, its ODI declined to USD 13 billion. Given that India is the 5th largest economy in the world, its ODI level is not commensurate with its economic position.

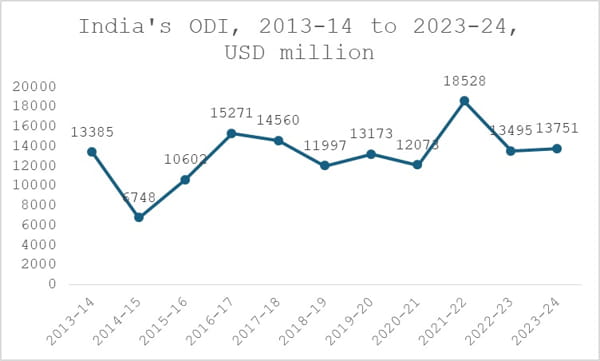

India’s ODI has remained rangebound over the last several years and the compound annual growth rate stood flat between 2013-14 (the earliest year for which data is available from Department of Economic Affairs, Ministry of Finance, India) and 2023-24. It is further characterized by large investments in certain years, which tend to make the flow lumpy.

Source: Department of Economic Affairs, Overseas Direct Investment, various years

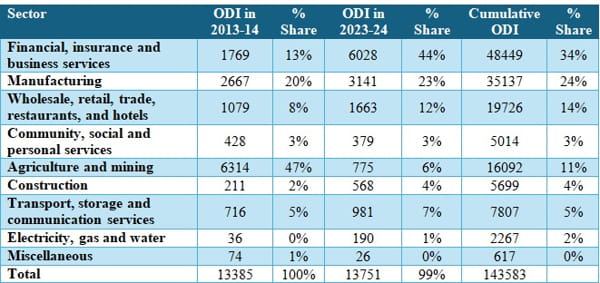

As per the Department of Economic Affairs, the sector of financial, insurance and business services accounted for 34% of the cumulative total ODI of USD 143.58 billion between 2013-14 and 2023-24. Manufacturing was the second most preferred sector with 24%, followed by wholesale, retail trade, restaurants and hotels sector. The agriculture and mining sector saw 11% of total cumulative ODI, with large investments in 2013-14 and 2017-18.

Share of Sectors in ODI, 2013-14 to 2023-24, USD million

Source: Department of Economic Affairs, Overseas Direct Investment, various years

A Strategic Indian Approach to Investments

In terms of countries, Singapore, the US, Mauritius, the Netherlands and UK were the top destinations. However, investments to some of these countries are likely to have been rerouted to other destinations.

From India’s perspective, several strategic considerations may inform the question of ODI policy.

First, the global economic footprint of a country has a major influence on its overseas heft. India’s Press Note 3 of April 2020 was aimed at curbing FDI from countries with which it shares a land border primarily due to security considerations. Likewise, India deploys overseas development assistance to expand its goodwill in partner countries. Similarly, overseas investments can play a key role in deepening India’s strategic presence.

From the business perspective, companies see significant advantages in leveraging overseas markets for growth. As per a report on subsidiaries of largest MNCs by revenue, the US accounted for a third of overseas subsidiaries with Japan and China in the next two slots. As many as 81 Indian companies had set up such subsidiaries, ranking 5th in the list. Many of the Indian companies which have ventured overseas find that their global operations have yielded better revenues than their domestic business.

Two, as a large developing economy, India is dependent on energy imports, which can be secured through investments in fields across the world. ONGC Videsh, the arm for overseas investments in oil and gas fields, has invested in 32 projects in 15 countries. Including other public sector enterprises in the oil and gas sector, India’s cumulative investments in exploration, production, development and pipelines adds up to USD 38 billion as of March 2023. Energy security investments would remain a major imperative for India to fuel its future growth.

Three, overseas investments would also drive India’s access to mineral resources and in particular, critical mineral resources, a vital raw material for emerging technology and sustainability sectors. India set up Khanij Bidesh India (KABIL) in 2019 as a government enterprise for sourcing critical minerals from overseas which has entered into agreements with various countries for investments and projects. To implement its Critical Minerals Mission, announced in the Indian Budget 2024-25, exploration and production in other countries including through ownership of mines would need to be considered. Similarly, acquiring mines in other countries can help India secure its supplies of copper ore, limestone, iron ore, and others, imports of which have risen considerably over recent years and are subject to commodity price volatility.

Four, it is increasingly imperative for India to undertake overseas investments for the purposes of scaling up technology adoption of its enterprises. Acquiring technology is one of the key reasons that companies invest overseas and at a time when Industry 4.0 technologies such as machine learning, Internet of Things, robotics and artificial intelligence are transforming manufacturing, India’s future industry competitiveness depends on alignment with this trend. Indian corporations have expanded investments for information and communication technologies (ICT). Key investments have also been made in the manufacturing sector, hotels, energy, and so on, which would additionally result in acquiring foreign know-how for driving global competitiveness. In many cases, smaller Indian manufacturers need to catch up in technology, while larger firms can enter into high-tech, high value-addition areas. With technology as a critical determinant for national progress and economic security, policy encouragement for technology related ODI would be increasingly relevant for India.

Five, overseas presence supports participation in global value chains (GVC) by building backward and forward linkages. About 70% of global trade takes place through such supply chains that witness movement of products and services from country to country, driving growth and job creation as well as productivity and know-how. India’s share in global exports is about 1.8% with share in high-tech sectors such as electronics and machinery at below 0.5%. While attracting FDI has been seen as a key policy measure for India’s higher integration into GVCs, the reverse is also necessary for expanding its trade presence at a time when these value chains are being diversified and restructured.

Six, while India is a global leader in Mode 1 services delivered online, the larger share of global services exports comes from Mode 3 or services delivered through commercial presence overseas which accounted for about 56% of aggregate services exports in 2022. Mode 1 services exports, on the other hand, contributed about 35%. The Indian trade profile reveals Mode 1 digital services exports at 74% of the total, with commercial presence overseas under Mode 3 services at just 14%. If India is to boost its services exports considerably, Indian companies would need to enhance their overseas presence.

Seven, ownership of critical infrastructure projects overseas would help to serve India’s strategic needs. India has invested in ports in Chabahar, Sittwe, Colombo West Terminal and Haifa, and also undertaken rail projects in several countries including Morocco, Malaysia and Sri Lanka. There is scope to build a stronger footprint overseas in sectors such as roads and highways, real estate and construction, industrial parks, and so on through investments.

Eight, ODI will build India’s strategic presence in the Global South. India’s experience of lines of credit for developmental projects and operations of Indian companies in African markets have underscored its collaborative model of business which takes into account local needs and local talent. Indian industry has so far preferred to invest in advanced markets even as emerging markets are growing faster.

Palk Strait Bridge, an India-Sri Lanka project | Organiser

The country has progressively liberalized its overseas investment regulations which are governed by the Foreign Exchange Management (Overseas Investment) Rules 2022. This introduced the concept of strategic sectors for the first time and eased ODI and overseas portfolio investments. Overseas Direct Investment is defined as acquisition of unlisted equity capital of a foreign entity, investment in 10% or more of paid-up capital of a listed foreign entity or acquisition with control of a listed foreign entity. As per the Master Direction issued by the Reserve Bank of India in July 2024, strategic sectors are currently defined to include energy, natural resources and startups enjoy special provisions.

Investments as a component of Economic Security

In today’s context, restrictions on foreign investment inflows are being imposed by several countries, making the global investment environment increasingly uncertain. Investment screening mechanisms in OECD countries have doubled over the last decade to reduce dependence on foreign investors in critical sectors, maintain technology leadership, and address geopolitical tensions. This is reflective of the security considerations in investment flows for both home countries and host countries.

For India to boost external investments in line with its rising economic growth, it should promote and encourage enterprises to look at overseas opportunities. Reinstating the bilateral investment treaties, which afford investor protection, as contemporary agreements that build confidence of investors on both sides would help to boost both inward and outward investment flows.

India should also look at setting up a sovereign wealth fund that could target strategic investments in key technologies, critical minerals, infrastructure projects and commercial ventures. Further, guarantees and credit facilities for overseas investments could be expanded for businesses. Public sector enterprises can also be supported to undertake more projects and ownership of foreign assets in these areas.

In the context of increasing geopolitical tensions, where trade and investment are increasingly being repurposed from business decisions to instruments being wielded for national security, enhancing external engagement and expanding overseas investments emerge as critical imperatives for advancing India’s strategic interests.

(Exclusive to NatStrat)

How Neighbouring Countries' Debt Crises Are Reshaping India's Foreign Policy

From Summits to Structures: Rethinking the India-Africa Partnership

Cyber Deterrence in the Indian Context: Constraints, Credibility and Escalation Risks

A National Economic Security Doctrine: Defining India’s External Engagement